The Hidden Cost of Disconnected Lending Data

Banks, credit unions, LOS providers, and lending technology teams do not need to be told that lending is data-intensive. Every application, decision, stipulation, verification step, exception, and portfolio outcome is shaped by the quality, availability, and usability of the data surrounding it.

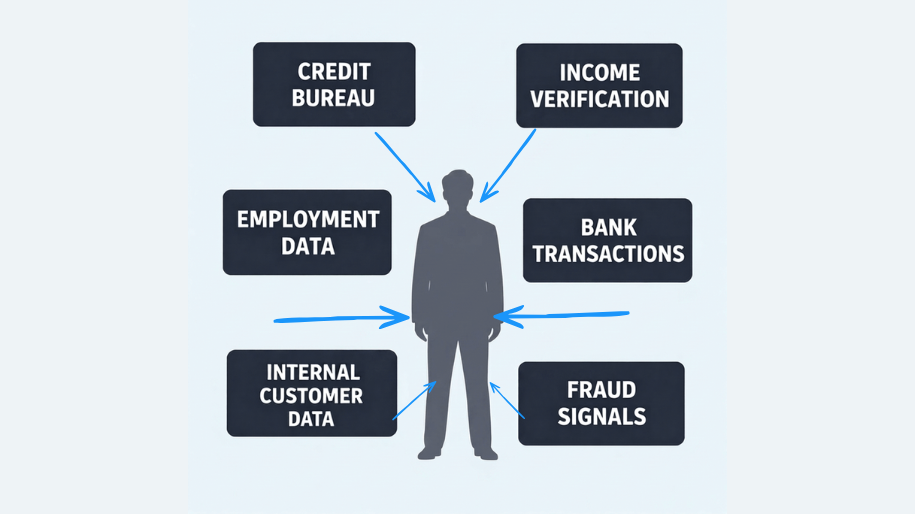

The issue is no longer whether financial institutions have access to data. Most already do. Credit data, income and employment data, transaction data, application data, internal customer or member data, document-based information, fraud indicators, and third-party data sources all exist somewhere within the lending ecosystem.

The more important issue is whether that data can be brought together and applied in a way that improves lending outcomes without creating additional operational burden.

That is where many institutions continue to face friction. Data may be available, but not always usable at the right moment. It may be held in one system, required in another, reviewed by a different team, or surfaced too late in the process to materially improve the decision. It may support one part of the workflow while remaining disconnected from the broader borrower picture.

This fragmentation is costly precisely because it is often absorbed into the normal course of lending operations. It appears as additional review, repeated documentation requests, manual reconciliation, inconsistent visibility across teams, longer cycle times, and missed opportunities to identify qualified borrowers already present in the application pipeline.

The cost is not simply technological. It is operational, commercial, and strategic.

Data silos remain a material barrier

The persistence of disconnected data is well documented across financial services. Salesforce, citing MuleSoft’s Connectivity Benchmark research, reported that 81% of IT leaders in financial services believe data silos are hindering digital transformation. The same article points to the broader challenge of fragmented systems and disconnected data in banking, particularly where institutions are trying to improve customer experience, decision-making, and operational agility.

This matters in lending because digital transformation is not abstract. It is judged in the quality and speed of the borrower experience, the consistency of decisioning, the efficiency of operations, and the institution’s ability to identify profitable lending opportunities without taking on unnecessary risk.

For credit unions and community or mid-market banks in particular, the challenge is often not ambition. Many are actively investing in modernization, automation, analytics, and better borrower experiences. The constraint is that data infrastructure and workflow realities do not always make it easy to apply the right data at the right point in the lending process.

The result is a gap between the data an institution can theoretically access and the value it can practically extract from that data.

More data does not automatically mean better decisions

The lending market has become increasingly focused on expanded data access. That focus is understandable. Alternative and permissioned data can help lenders better assess income, employment, cash flow, affordability, stability, and borrower behaviour, particularly where traditional credit data may provide an incomplete view.

Conductiv’s own guide to alternative credit scoring discusses how non-traditional data can support a broader understanding of borrower creditworthiness, while its page on AI lending solutions for credit unions references data inputs such as bank transaction history, verified income, and employment tenure in the context of thin-file and credit-invisible members.

However, expanded data access only creates value when the data can be operationalized. Adding more sources to an already fragmented environment can increase complexity if those sources are not connected to the workflows, policies, systems, and decision points that determine lending outcomes.

This is why the more useful question is not only, “What other data could we bring in?” It is also, “How effectively are we using the data already available to us?”

For many institutions, there is meaningful value locked inside existing borrower, member, application, transactional, and performance data. There may also be value in third-party and permissioned consumer data that is available but underused because of integration, workflow, vendor, or operational constraints. The opportunity lies in connecting those sources in a way that makes them actionable without adding unnecessary process complexity.

The practical problem is usability

A data source can be accurate, relevant, and valuable, yet still have limited impact if it is not usable in the lending process. If it arrives too late, requires too much manual interpretation, sits outside the primary workflow, or cannot be evaluated alongside other relevant borrower information, its value is reduced.

This is one of the central challenges for lenders. Lending teams are often not lacking individual data points; they are lacking a complete and timely view that allows those data points to be considered together. Credit performance, verified income, employment stability, transaction behaviour, internal relationship history, application data, and risk indicators all become more useful when they contribute to a connected borrower picture.

When that connected picture is missing, teams compensate in familiar ways. They request more documentation, apply additional review, move between systems, manually reconcile inconsistencies, or make decisions using the subset of information that is most readily available. None of this is unusual, and much of it is embedded in standard operating practice. But over time, these workarounds create friction that affects speed, cost, consistency, and borrower experience.

This is where data orchestration becomes strategically important. In a lending context, orchestration is not about accumulating more data for its own sake. It is about making relevant data accessible, connected, contextualized, and actionable inside the workflows and existing systems where lending decisions are made.

The borrower experience is shaped by backend data realities

Borrowers and members do not experience data fragmentation as a systems issue. They experience it as delay, repetition, uncertainty, or unnecessary friction. They may be asked for information they believe the institution already has, asked to verify details through a separate process, or left waiting while teams reconcile information across systems and providers.

This matters because expectations around financial services experiences continue to rise. Borrowers increasingly expect lending processes to be clear, fast, and digitally intuitive. For credit unions, the member experience is also closely tied to trust, service, and relationship value. For banks and other lenders, process friction can affect completion rates, conversion, and competitive positioning.

The institution may see disconnected data as an operational challenge. The borrower experiences it as part of the brand.

That is why improving data usability is not only a back-office concern. It directly affects the quality of the lending experience and the institution’s ability to compete for qualified borrowers.

Automation and AI raise the stakes

As financial institutions invest further in automation, analytics, and AI-enabled lending capabilities, the importance of usable data increases. These technologies can only perform as well as the data environment that supports them. If relevant data remains fragmented, delayed, poorly structured, or difficult to interpret within the lending workflow, then automation may simply accelerate an incomplete process rather than improve it.

McKinsey has argued that banks seeking to capture value from AI need to rewire the enterprise rather than treat AI as a series of isolated use cases. Its analysis points to the importance of aligning data, technology, operating models, and workflows so that AI can create value at scale. That point is highly relevant to lending because the value of analytics or automation depends not only on the sophistication of the model, but on the quality and accessibility of the data being applied.

The same principle applies even outside AI. Better data does not replace lending judgment, risk policy, or institutional expertise. It strengthens them by giving teams a more complete and timely basis for action.

The opportunity is to unlock value already present in the lending ecosystem

The hidden cost of disconnected lending data is not always visible in a single metric. It is distributed across manual work, review queues, borrower friction, inconsistent visibility, delayed decisions, underused data sources, and opportunities that are never fully evaluated.

For lenders, the opportunity is to look beyond data access alone and focus on data usability. Can internal borrower and application data be combined more effectively with permissioned consumer data? Can third-party sources be applied without creating avoidable vendor and integration complexity? Can income, employment, transaction, credit, and risk signals be evaluated together in a way that supports the existing lending process? Can better data improve decision quality without requiring teams to abandon the infrastructure and workflows they already use?

These are not theoretical questions. They sit at the centre of how lenders improve efficiency, strengthen borrower assessment, expand access responsibly, and compete in an increasingly data-driven market.

The future of lending will not be defined by which institution has the most data. It will be defined by which institutions can turn relevant data into timely, useful, and confident lending decisions.

How Conductiv helps

Conductiv helps credit unions, banks, and lenders access, aggregate, and operationalize data within existing lending workflows.

By bringing together internal borrower and application data, permissioned consumer data, and relevant third-party sources, Conductiv helps institutions create a more complete and usable view of the borrower. That data can then support the lending systems, decisioning tools, scoring models, and workflows already in place.

Conductiv is designed to strengthen existing lending infrastructure by improving the quality, completeness, and usability of the data that feeds into it. For lending teams, this means less reliance on disconnected systems, fewer unnecessary manual steps, and a more practical way to apply data where it can influence decisions.

For lenders, the question is not simply whether more data exists. The question is whether the data available to them can be used well enough to support better lending decisions.